The People’s Bank of China (PBOC) maintains a rigid Loan Prime Rate (LPR) not out of systemic complacency, but as a calculated response to a trilateral constraint involving net interest margins (NIM), currency stability, and the diminishing marginal utility of credit expansion. While market spectators often interpret a "hold" on rates as a pause in stimulus, it is more accurately defined as a tactical redirection of liquidity. Beijing has shifted from broad-spectrum interest rate cuts to a targeted quantitative easing framework, signaling that the floor for the Chinese Yuan (CNY) has become a higher priority than the cost of corporate borrowing.

The Trilateral Constraint Framework

To understand why the one-year and five-year LPR remain unchanged, one must analyze the three competing pressures currently paralyzing the PBOC’s conventional toolkit.

1. The Net Interest Margin (NIM) Floor

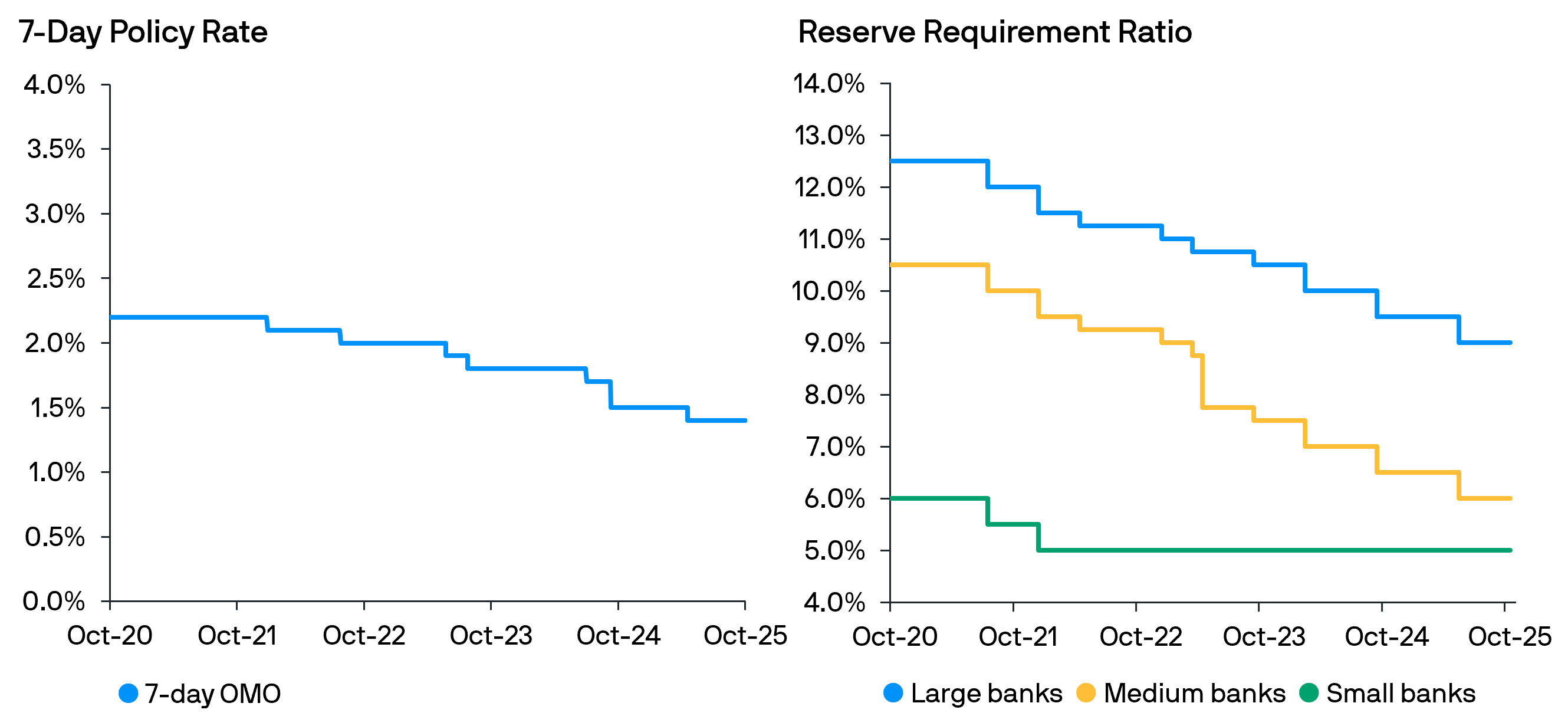

Chinese commercial banks are facing record-low net interest margins, hovering near 1.5%. For a banking system to remain solvent and capable of absorbing non-performing loans (NPLs) within the property sector, a specific spread must be maintained between deposit liabilities and loan assets.

- The Compression Mechanism: When the PBOC lowers the LPR without a commensurate drop in deposit rates, bank profitability evaporates.

- The Stability Risk: If margins fall below the critical threshold required for capital adequacy, the banking system's ability to provision against bad debts in the real estate sector is compromised.

2. The Interest Rate Differential and Capital Outflow

The divergence between the U.S. Federal Reserve’s "higher for longer" stance and China’s deflationary environment creates a persistent yield gap. This gap exerts downward pressure on the Yuan as capital seeks higher returns in dollar-denominated assets.

- The Currency Floor: A weaker Yuan increases the cost of imported commodities and risks triggering a flight of domestic capital. By holding the LPR steady, the PBOC is effectively defending the 7.2-7.3 USD/CNY corridor.

- The Signaling Effect: Keeping rates unchanged signals to global markets that Beijing will not sacrifice the currency to chase incremental GDP growth through debt.

3. The Liquidity Trap and Credit Elasticity

Lowering the cost of money is only effective if there is a demand for credit. Current data suggests that Chinese private enterprises and households are focused on deleveraging rather than expansion—a classic liquidity trap.

- The Elasticity Problem: Reducing the LPR by 10 or 20 basis points does not stimulate borrowing if consumer confidence is anchored by falling property values.

- The Misallocation Risk: Excessively cheap credit in a low-demand environment often results in "zombie" lending or speculative bubbles in the bond market rather than productive capital expenditure.

The Pivot to Quantitative Tools and Reserve Requirements

The decision to hold the LPR indicates a transition in the PBOC's operational manual. Instead of adjusting the price of money, the central bank is now focused on the quantity of money and the velocity of its circulation.

Structural RRR Reductions vs. LPR Cuts

The Reserve Requirement Ratio (RRR) has become the primary lever for injecting liquidity. By lowering the RRR, the PBOC frees up bank capital for lending without directly hitting the interest income of the banks. This serves as a "stealth stimulus" that provides the banking system with the liquidity needed to support government bond issuances, which are essential for fiscal spending on infrastructure.

Targeted Re-lending Programs

Rather than a blanket rate cut that benefits all sectors indiscriminately, the PBOC is utilizing targeted re-lending facilities. These are directed specifically toward:

- High-end Manufacturing: Upgrading the industrial base to move up the value chain.

- Green Energy: Supporting the transition to a low-carbon economy.

- Property Sector "White Lists": Providing credit strictly to viable housing projects to ensure delivery to buyers, preventing systemic contagion.

Currency Tolerance and the Export Paradox

Beijing’s signaled tolerance for a stronger Yuan, or at least its refusal to allow further depreciation, creates a paradox for its export-led recovery. Traditionally, a weaker currency aids exports. However, China is currently prioritizing the "Internationalization of the RMB" and the stability of its balance of payments.

The "Strong Yuan" signal serves two strategic functions:

- Imported Inflation Mitigation: It keeps the cost of energy and raw materials manageable for manufacturers.

- Foreign Investment Retention: Stability in the exchange rate reduces the "currency risk" for foreign institutional investors holding Chinese sovereign debt.

The cost of this stability is a reduction in the price competitiveness of Chinese exports on the global stage. However, the leadership appears to have calculated that the risk of a disorderly currency devaluation—leading to massive capital flight—is a far greater threat than a slight cooling in export volumes.

The Fiscal-Monetary Coordination Bottleneck

The effectiveness of holding interest rates steady depends entirely on the synchronization between the PBOC and the Ministry of Finance. Monetary policy in China is currently in a "supportive" role rather than a "leading" role.

The bottleneck is no longer the availability of credit, but the speed of fiscal deployment. If the central government issues special bonds to fund regional projects, the PBOC must ensure the banking system has enough liquidity to purchase those bonds without spiking market interest rates. This is why the Medium-term Lending Facility (MLF) and LPR are being held stable; the PBOC is waiting for the fiscal side to create the demand that monetary policy can then facilitate.

The Real Estate Debt Overhang

The five-year LPR is the primary benchmark for mortgages. The refusal to cut this rate further reflects a desire to avoid re-inflating the property bubble. The strategy is now "management of decline" rather than "revival." By keeping the five-year rate steady, the PBOC is forcing a slow deleveraging process, preventing a "Minsky Moment" where a sudden collapse in asset values triggers a systemic financial crisis.

Strategic Tactical Recommendation: The Credit Quality Shift

Investors and analysts should stop monitoring the LPR as the definitive barometer of Chinese economic health. It has become a lagging indicator, constrained by international FX pressures and domestic bank margins.

The superior metric for the next 12 months is the Total Social Financing (TSF) composition. Specifically, track the ratio of government bond issuance to corporate lending. A rise in the former, supported by RRR cuts and stable LPR, indicates a transition to a state-led investment model designed to bypass the paralyzed private property market.

For entities operating within China, the strategic play is to align capital structures with the PBOC’s "targeted" sectors—advanced manufacturing and "new energy"—where credit is being funneled through non-rate channels. Expect a period of "horizontal" interest rate movement accompanied by "vertical" liquidity injections in high-priority industrial verticals. The defense of the Yuan is not a temporary posture; it is the structural anchor of the current Five-Year Plan's financial stability mandate.