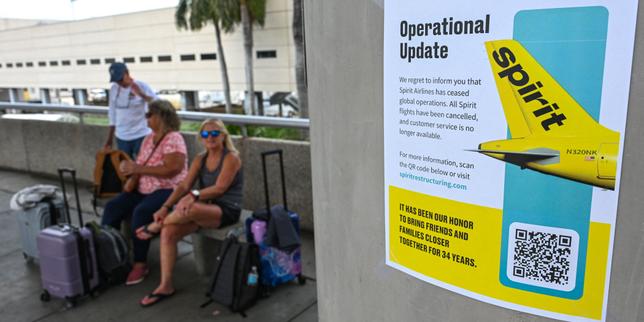

The cessation of Spirit Airlines’ operations represents the systemic failure of the Ultra-Low-Cost Carrier (ULCC) model in a post-pandemic economic environment. While superficial analyses attribute this collapse to mere debt accumulation, the reality is a fundamental mismatch between fixed operational costs and a decaying revenue-per-available-seat-mile (RASM) framework. Spirit did not just run out of cash; it ran out of viable airspace in a market where the cost of complexity now outweighs the efficiency of "unbundling."

The Unit Cost Paradox and the Erosion of Margin

The ULCC thesis relied on the principle of the lowest possible Cost per Available Seat Mile excluding fuel (CASM-ex). Historically, Spirit maintained a significant spread between its costs and those of legacy carriers like Delta or United. This spread has narrowed to the point of irrelevance due to three specific inflationary pressures.

- Labor Arbitrage Reversal: The 2023-2024 pilot and flight attendant contract cycles across the industry reset the baseline for wages. Spirit, previously benefiting from lower labor costs, saw its CASM-ex spike as it was forced to match industry standards to prevent a total talent exodus.

- Maintenance Tailwinds Turned Headwinds: The Pratt & Whitney GTF engine issues forced the grounding of a substantial portion of Spirit’s A320neo fleet. In a high-utilization model, a grounded aircraft is not just a lost asset; it is a fixed-cost anchor. The lack of operational redundancy meant Spirit could not absorb the loss of capacity while still servicing its debt.

- Capital Structure Rigidity: Unlike legacy carriers with diverse asset bases, Spirit’s balance sheet was heavily geared toward high-leverage lease agreements. When interest rates climbed, the cost of refinancing $1.1 billion in loyalty-program-backed loyalty bonds became prohibitive.

The Revenue Ceiling of the Unbundled Model

Spirit’s revenue strategy was predicated on the "unbundling" of services—charging a base fare and layering ancillary fees for bags, seats, and water. This model hit a ceiling caused by a shift in consumer psychology and competitive counter-maneuvers.

Legacy carriers introduced "Basic Economy," which effectively weaponized Spirit’s own strategy against it. By offering a stripped-down fare with the perceived reliability and network breadth of a major airline, legacy carriers captured the price-sensitive traveler. Spirit’s primary differentiator—the lowest price—was neutralized.

The "Ancillary Dependency" also reached a point of diminishing returns. There is a physiological and psychological limit to how many fees a passenger will accept before the friction of the transaction outweighs the savings. As total travel costs (base fare + fees) approached the price of a bundled ticket on a mid-tier carrier like JetBlue or Southwest, Spirit’s value proposition vanished.

The Failed Merger as a Catalyst for Liquidation

The Department of Justice’s block of the JetBlue-Spirit merger was the definitive inflection point. The merger was not a growth play; it was a survival maneuver designed to pivot Spirit’s assets into a higher-yielding "premium-leisure" segment.

- Network Incompatibility: Spirit’s point-to-point network was optimized for high-utilization, leisure-heavy routes (e.g., Fort Lauderdale to Orlando). These routes are the first to suffer during a capacity glut.

- Asset Liquidity: Without the merger, Spirit was left with a fleet of A320s that were depreciating in real-world utility due to the aforementioned engine issues. The inability to merge meant Spirit could not scale its way out of its debt-to-EBITDA ratio, which had ballooned to unsustainable levels.

The Three Pillars of ULCC Failure

To understand why Spirit could not be restructured in its current form, we must examine the breakdown of the three pillars that once supported its growth.

1. Operational Homogeneity

The strength of a ULCC is a single aircraft type. This reduces training costs and spare parts inventory. However, when a systemic manufacturing flaw (like the GTF engine issue) hits that single aircraft type, the entire airline is paralyzed. Spirit’s lack of fleet diversity transformed from a cost-saving measure into a single point of failure.

2. High Asset Utilization

Spirit’s profitability required planes to be in the air 12+ hours a day. Any disruption—ATC delays, weather, or maintenance—cascades through the system because there are no "spare" aircraft. As the US airspace became more congested and the FAA implemented stricter flow controls, Spirit’s ability to maintain high utilization collapsed. The resulting "recovery costs" (rebooking passengers on other airlines or providing hotels) frequently exceeded the revenue generated by the flight itself.

3. Secondary Airport Strategy

Spirit often flew to secondary airports with lower landing fees. However, as legacy carriers consolidated hubs and optimized their own regional networks, the cost savings of secondary airports were eclipsed by the lack of "feeder" traffic. Spirit was forced to compete in primary markets (like Newark or O'Hare) where landing fees are high and competition is predatory.

The Mechanistic Reality of Bankruptcy

The cessation of activities indicates that the airline reached a "Covenant Breach" state. Once the cash on hand fell below the thresholds required by its credit card processors and bondholders, the processors began withholding "holdbacks"—the cash from ticket sales—to protect themselves against potential refunds. This created a terminal liquidity squeeze.

A Chapter 11 reorganization requires a "debtor-in-possession" (DIP) financing lead. If no lender believes the airline can return to profitability in its current ULCC configuration, the only path is Chapter 7 liquidation or a "Section 363" sale of its assets (slots, gates, and planes) to the highest bidder.

The Macro-Economic Shift in Leisure Travel

The market has moved from "Price First" to "Value First." The "revenge travel" surge of 2022-2023 saw consumers willing to pay a premium for reliability and comfort. Spirit’s brand equity was deeply tied to "cheap," which became a liability when consumers prioritized the "experience."

Furthermore, the rise of remote work changed the seasonality of travel. The traditional "peaks" and "valleys" flattened, but Spirit’s model was built to exploit those peaks. In a flatter demand environment, the legacy carriers’ ability to capture high-yield corporate travelers on the same aircraft as leisure travelers provides a diversified revenue stream that a pure-play ULCC cannot match.

Strategic Forecast for the Remaining Market

The liquidation of Spirit Airlines marks the end of the first generation of American ULCCs. The remaining players, such as Frontier and Allegiant, face an immediate choice: evolve or expire.

- Asset Realignment: Expect a massive sell-off of A320neo delivery slots. These will likely be snapped up by legacy carriers or international leasing firms, further concentrating market power.

- The Hub-and-Spoke Dominance: The exit of Spirit will lead to an immediate 15-20% increase in fares on leisure-heavy routes where Spirit was the primary price floor.

- Niche Specialization: The only path forward for low-cost carriers is "Ultra-Niche" (Allegiant’s model of connecting small towns to vacation destinations) rather than "Ultra-Low-Cost" (Spirit’s model of flying high-density routes).

The primary strategic move for investors and competitors is to identify the specific geographic voids left by Spirit's exit—specifically in the Caribbean and Latin American corridors—and move to secure those gates. However, any carrier attempting to fill the void using the same "high-utilization, unbundled" logic will meet the same fate. The cost of labor and the volatility of engine technology have made the $29 fare an economic impossibility. The industry is returning to an era of "Rational Capacity," where the price of the ticket must finally reflect the true cost of the operation.