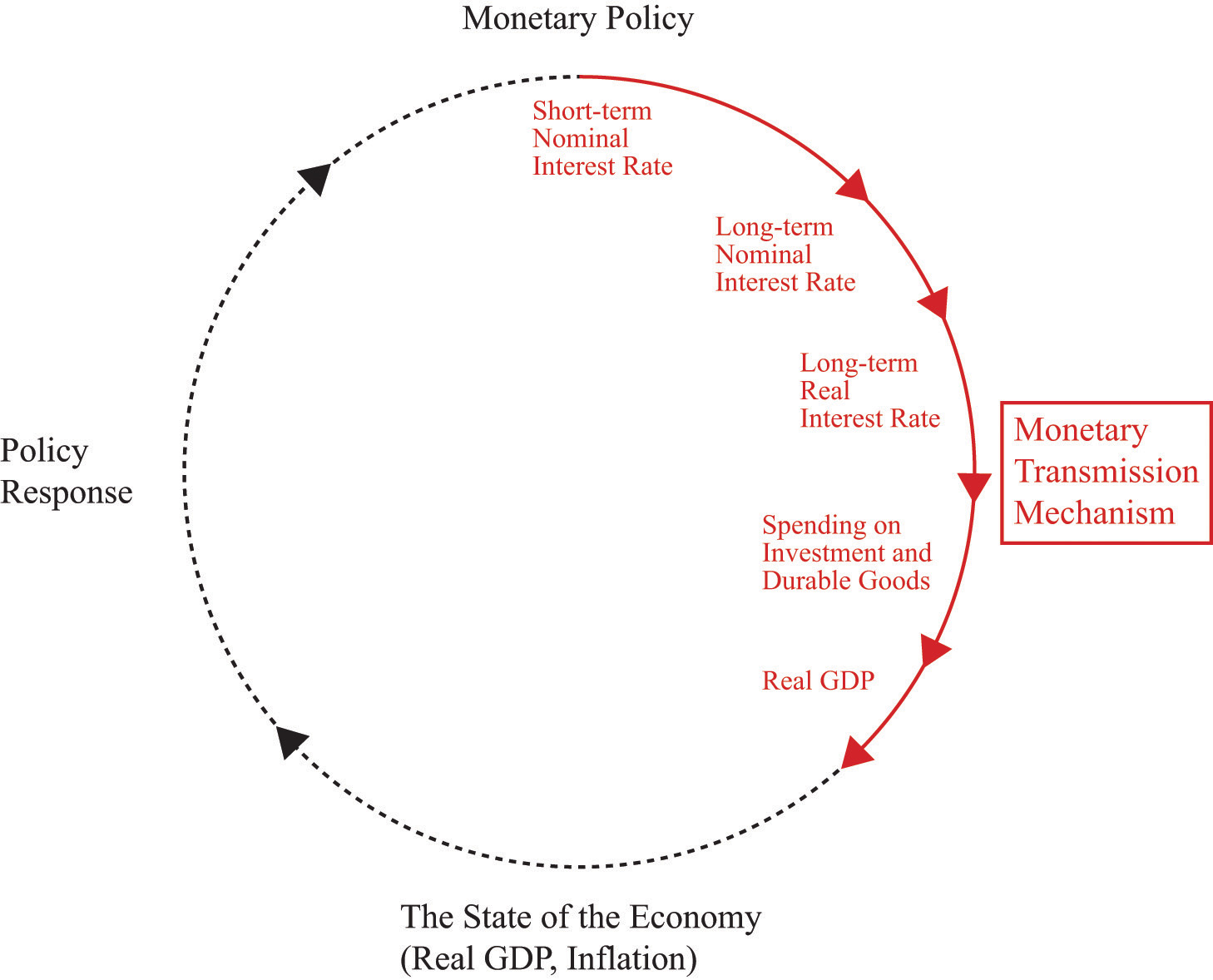

The Federal Reserve’s decision to reduce the federal funds rate in December functions as a catalyst for a multi-layered realignment of the American credit system. While surface-level analysis focuses on the immediate "relief" for consumers, a structural deconstruction reveals a complex transmission mechanism where the speed of interest rate pass-through varies wildly across different asset classes. The efficacy of this rate cut depends entirely on the spread between the federal funds rate and specific commercial benchmarks, a gap often dictated by bank liquidity requirements and institutional risk appetite rather than simple central bank fiat.

The Hierarchy of Interest Rate Pass-Through

The impact of a Fed rate cut is not uniform. It follows a chronological and structural hierarchy determined by the "closeness" of a financial product to the overnight lending markets.

- Direct Transmission (Immediate): Products tied directly to the Prime Rate, such as Credit Cards and Home Equity Lines of Credit (HELOCs).

- Lagged Transmission (Intermediate): Auto loans and short-term personal credit, which respond to shifts in the 2-year Treasury yield.

- Disconnected Transmission (Speculative): 30-year fixed-rate mortgages, which track the 10-year Treasury yield and long-term inflation expectations rather than the short-term federal funds rate.

Credit Cards and the Prime Rate Margin

Credit card Annual Percentage Rates (APRs) represent the most efficient transmission of Fed policy. Most revolving credit accounts are indexed to the Prime Rate, which typically sits 3 percentage points above the federal funds target range. When the Fed moves, the Prime Rate moves in lockstep, usually within one to two billing cycles.

However, the 25 or 50 basis point reduction in December does not fundamentally alter the debt trap for high-balance carryovers. With average APRs hovering near record highs, a fractional decrease offers negligible mathematical relief. For a balance of $10,000 at a 24% APR, a 0.25% cut reduces the monthly interest charge by approximately $2.08. The real strategic value of the December cut for credit card holders lies not in the interest reduction, but in the potential for "balance transfer" windows to reopen as banks compete for higher-quality borrowers in a lower-rate environment.

Mortgage Rates and the 10-Year Treasury Yield

Mortgage markets operate through a distinct transmission mechanism that many homeowners and prospective buyers misunderstand. The 30-year fixed-rate mortgage is essentially a bet on the 10-year Treasury yield, which reflects long-term economic outlooks and inflation expectations.

The December rate cut has a counter-intuitive relationship with mortgage rates. If the market interprets the Fed's move as a sign of economic weakness, 10-year yields may fall, dragging mortgage rates lower. However, if the market perceives the cut as potentially inflationary, the 10-year yield may rise, paradoxically increasing the cost of 30-year fixed mortgages despite the Fed's accommodative stance.

The primary variable for current mortgage holders is the "break-even point" for refinancing. A rate cut of 0.25% or 0.50% is rarely enough to justify the closing costs of a new loan, which typically range from 2% to 5% of the total loan amount. The structural math for a refinance requires a rate drop of at least 0.75% to 1.0% to be viable over a three-to-five-year time horizon.

Auto Loans and Personal Debt Consolidation

Unlike the 30-year mortgage, auto loans and personal debt consolidation products are more sensitive to short-to-intermediate-term credit market conditions. The December cut eases the funding costs for lenders, but the speed of transmission to the consumer is hindered by the current risk premium in the subprime and near-prime sectors.

- New Vehicle Financing: Large manufacturers often subsidize interest rates through their captive financing arms (e.g., Ford Credit). A December Fed cut allows these captives to offer lower "teaser rates" (0% to 2.9% APRs) more profitably.

- Used Vehicle Financing: These rates are determined more by the secondary market for asset-backed securities (ABS) and local credit union liquidity. Expect a three-to-six-month lag before the December rate cut meaningfully impacts the average used car loan.

The Savings Rate Compression and the Cash Yield Trap

The December rate cut is a net negative for savers and fixed-income investors. High-Yield Savings Accounts (HYSAs) and Certificates of Deposit (CDs) respond quickly to a lower federal funds rate as banks seek to reduce their cost of capital.

The "yield trap" emerges when investors fail to lock in rates before the Fed's policy shift. HYSAs are variable-rate products and can be adjusted downward by banks within 24 hours of a Fed announcement. In contrast, CDs lock in a fixed rate for a specific term. The strategic response to the December cut is a rapid migration from liquid cash accounts into short-term (6-month to 12-month) CDs to preserve yield before the broader market resets.

Student Debt and Variable vs. Fixed Federal Rates

The impact on student debt is bifurcated by the type of loan:

- Federal Student Loans: These rates are set annually by Congress based on the 10-year Treasury note auction in May. The December rate cut will have zero impact on current federal loans but could influence the rates for loans disbursed for the following academic year (starting July 1).

- Private Student Loans: These are often variable-rate products tied to the Secured Overnight Financing Rate (SOFR) or the Prime Rate. Borrowers in this category will see an almost immediate reduction in their monthly interest charges, mirroring the transmission seen in credit cards.

Structural Constraints and the "Sticky" Inflation Variable

The effectiveness of the December rate cut is constrained by the "stickiness" of service-sector inflation. If the Fed cuts rates while inflation remains above the 2% target, real interest rates (the nominal rate minus inflation) could become negative, eroding the purchasing power of cash even as borrowing costs decline.

The December move is a signal of a shift in the "neutral rate"—the interest rate that neither stimulates nor restricts economic growth. If the neutral rate is higher than previously estimated, the Fed may find itself unable to cut rates as aggressively as the market expects throughout the following year. This creates a "higher-for-longer" floor that prevents borrowing costs from returning to the historic lows of the previous decade.

The Strategy for Capital Allocation

To navigate the post-December rate environment, capital allocation must be proactive rather than reactive. The primary strategic play involves prioritizing the liquidation of high-interest revolving debt, which remains expensive despite the fractional rate cut.

The secondary play is the management of liquidity. With the downward trend in HYSA yields, shifting capital toward short-term Treasury bills or fixed-income instruments offers a way to capture the remaining yield before the Fed’s easing cycle continues.

Finally, for those looking to enter the housing market, the December cut is less a reason to buy and more a signal to monitor the spread between the 10-year Treasury and mortgage rates. If this spread narrows, it indicates a return to market stability, providing a more reliable entry point than the volatile period immediately following a Fed announcement.

The structural reality of the December rate cut is that it is a directional shift, not a destination. Its primary value is psychological—it resets expectations for the cost of capital, but its mathematical impact on the individual balance sheet will be measured in years, not months.